In personal finance, many people focus on micro-expenses, like a daily coffee, or that monthly visit to lululemon, as the primary obstacle to wealth.

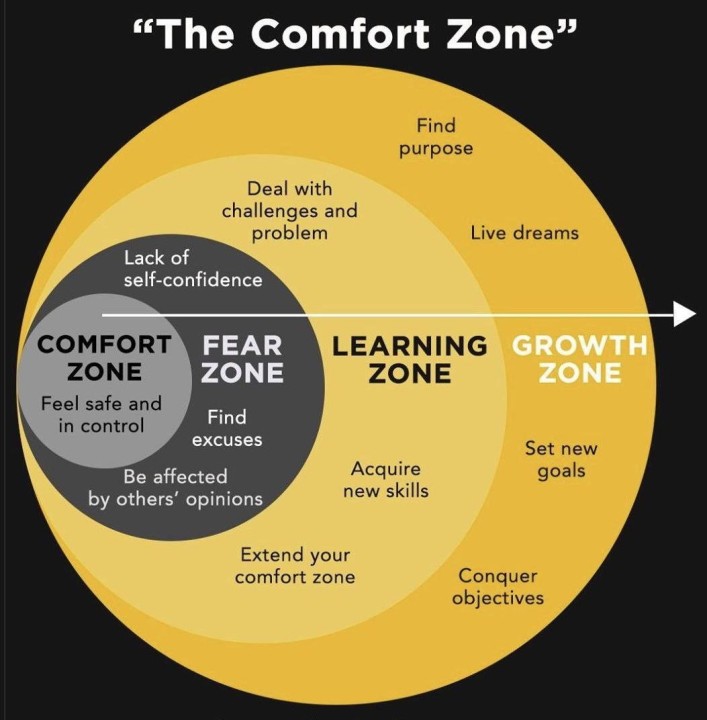

While not untrue, the far greater and more common financial danger is the comfort zone. This isn't just a psychological bubble; it's the "safe" path we were actively taught to pursue. It’s the script we learned growing up: study hard, get a stable job, save your money, and don't take "risky" actions.

This "safe" bubble of familiar routines and default choices feels secure, but it is also the primary barrier to meaningful financial growth. In finance, a lack of growth is a guaranteed loss against inflation and opportunity cost.

Identifying the High-Risk "Comfort Zones" in Investing

This financial inertia often manifests in several common, high-risk behaviours.1. Professional Stagnation

This is the "safe and stable" job, the "iron rice bowl". While the pay is predictable, there is an implicit understanding that the salary from a "safe and stable" job will never make you wealthy. Furthermore, most people in these jobs find themselves stagnant with no new or valuable skills acquired in years. The "comfort" of stability and the inertia of avoiding the job hunt prevent action, directly capping income potential.2. The "Safe Money" Trap (Analysis Paralysis)

This behaviour involves holding significant capital — $50,000, $100,000, or more — in a standard savings account. While this "feels" safe, it is a position of guaranteed loss as inflation erodes its purchasing power every year. This is often a symptom of "analysis paralysis." The individual may have read numerous books and watched hours of content on investing but remains perpetually waiting for the "perfect time" or "perfect deal." They have mistaken research (comfort) for action (growth).3. Following the Default "Singapore Script"

This is the cultural default path: BTO, save for a condo, and work a 30-year 9-to-5 career. While a valid path, it's often followed without a critical analysis of whether it aligns with one's personal financial goals. The "comfort" of a pre-defined script eliminates the need to explore alternative and potentially far more profitable strategies, such as building scalable assets for cash flow.