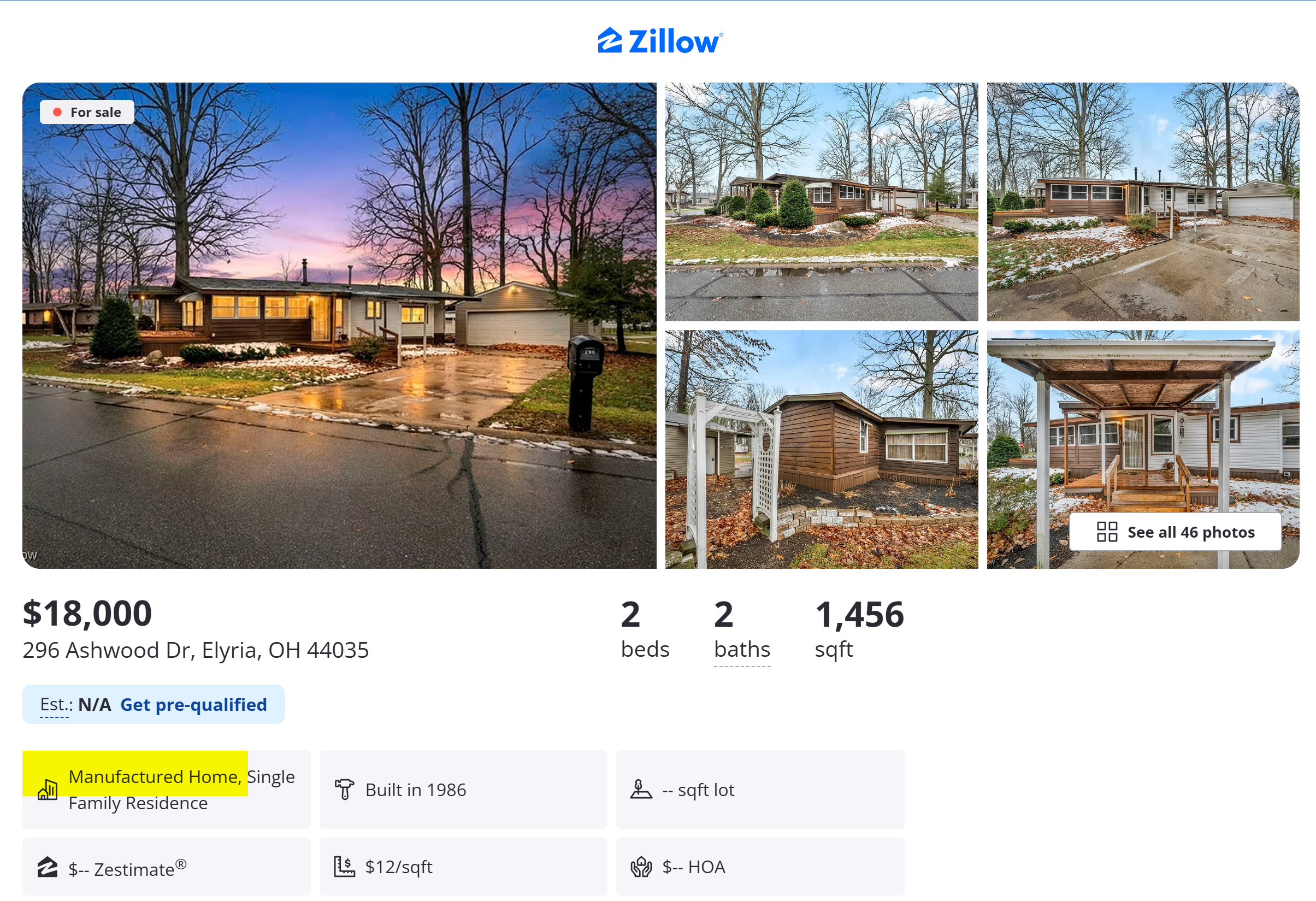

For many international property investors, the sight of a $18,000 "landed house" on Zillow feels like a glitch in the system. Coming from markets where entry-level property requires six or seven figures, it is tempting to view these manufactured or mobile homes as the ultimate high-yield opportunity. However, to build a resilient and scalable portfolio, you must look past the low entry price and understand the fundamental difference between owning an asset and owning a depreciating box.

The strategic path we use to build our 25+ property portfolio relies on forced appreciation and the ability to recycle capital. Mobile homes, while attractive on a spreadsheet for their initial cash flow, often fail this system because they lack the primary driver of real estate wealth: land ownership.

The Structural Distinction: VIN vs. Title

When you acquire a Single Family Home (SFH), you own both the structure and the land underneath it. In the US market, it is the land that appreciates over time, while the structure is simply the vehicle that produces rent. In contrast, a Mobile Home is built in a factory on a permanent chassis and issued a Vehicle Identification Number (VIN), much like a car.

For the remote investor, the red flag is simple to spot: if a property is priced at $20,000 while neighboring traditional homes are selling for $200,000, you are likely looking at a "Manufactured" home type. You are buying the structure, but you are renting the land (Lot Rent) from a land owner. You have effectively moved from being a landlord to also being a tenant of the land owner.

The Cash Flow Mirage: Why the Bad Outweighs the Good

On paper, the numbers are undeniable. You can acquire these units for a fraction of the cost of a traditional home, and the rent-to-price ratio can result in gross yields that far exceed the 10-12% we target for Single Family Homes. Taxes are also minimal because the asset is often taxed as personal property (a vehicle) rather than real estate.

However, the "Forever Expense" of lot rent creates a significant risk profile. Unlike a mortgage, which eventually disappears, lot rent is a permanent monthly cost that the land owner can increase at their discretion. If the land owner decides to sell to a developer, you may be forced to move the home — a process that is cost-prohibitive and can often compromise the integrity of older structures.

Why Mobile Homes Fail the BRRRR Model

The most critical reason we prioritize Single Family Homes over mobile homes is the ability to scale. To rapidly grow a portfolio, you must be able to perform a cash-out refinance to pull your capital back out. Mobile homes break this repeatable system for two reasons:

- Financing Limitations: Lenders rarely offer 30-year fixed mortgages on mobile homes without land. You are often restricted to "Chattel Loans" with higher interest rates and shorter terms.

- Depreciation: Traditional real estate allows you to force appreciation through strategic renovation. A mobile home, however, depreciates like a vehicle. You cannot easily manufacture equity to fund your next acquisition.

While large-scale investors make significant money by owning the Mobile Home Parks (the land itself), buying individual "boxes" on rented land often results in your capital being "stuck." It is a strategy that captures yield but sacrifices long-term wealth and scalability.

You can watch how we perform forced appreciation on our Single Family Homes and cash-out the equity to scale in this video.